Establishing a company in the UAE can be fast, but “fast” is exactly what makes many founders rush past details that later become expensive: the wrong license, a structure banks will not onboard, tax registrations missed, or visa plans that do not match the headcount you need.

This guide walks through the most common pitfalls when establishing company operations in the UAE, why they happen, and how to avoid rework.

Why UAE setups go wrong (even when the formation is approved)

A UAE company can be incorporated relatively quickly compared to many jurisdictions. The trap is assuming that incorporation equals operational readiness.

In practice, you are aligning multiple systems at once:

- Licensing rules (activities, office requirements, regulated approvals)

- Corporate structure (shareholders, UBO disclosure, governance)

- Banking and compliance expectations (KYC, source of funds, substance)

- Tax and bookkeeping requirements (corporate tax, VAT where applicable)

- Immigration (residency visas, renewals, dependent visas)

A misstep in one area tends to cascade into the others.

Pitfall 1: Choosing the wrong jurisdiction (or choosing too early)

One of the most common mistakes is picking a free zone or mainland license based primarily on a listicle, a friend’s recommendation, or the lowest advertised setup price.

At a high level, you typically choose between mainland, free zone, and (in some cases) offshore structures. The “best” answer depends on where you will trade, what you will sell, and what counterparties (clients, platforms, banks) will expect.

Here is a practical comparison to frame the decision.

| Option | Often best for | Common pitfall | What to validate early |

|---|---|---|---|

| UAE mainland | Serving UAE onshore clients, local contracting, retail/physical presence | Assuming you can avoid office requirements or regulated approvals | Permitted activities, office/ejari needs, sector approvals |

| UAE free zone | Cross-border services, e-commerce, regional HQ functions, specific clusters (media, tech, logistics) | Discovering too late that some clients require a mainland contract or local registration | Where customers are based, import/export needs, banking fit |

| Offshore (where relevant) | Holding, asset ownership, certain international structures | Trying to use it as an operating business with staff, visas, or UAE trading | Purpose (holding vs operating), compliance, banking reality |

If you are not sure which route aligns with your business model, start by mapping your actual operating needs rather than the incorporation steps. The UAE Ministry of Economy provides helpful context on doing business and corporate frameworks in the UAE on its official site: UAE Ministry of Economy.

Pitfall 2: Selecting activities that do not match how you really make money

Licenses are issued based on permitted activities. Founders sometimes pick a broad “consulting” activity to move quickly, then later discover that their real operations are closer to:

- marketing services vs media buying

- software development vs IT consultancy

- e-commerce vs trading vs brokerage

- education/training vs professional services

This matters because the activity affects approvals, office requirements, and banking risk assessment.

Two common failure patterns:

- Activity mismatch shows up during banking. Banks compare invoices, contracts, website, and actual flows against the licensed activity. A mismatch can lead to delays, additional questions, or rejection.

- Regulated activities get missed. Certain sectors can require extra permissions (for example, financial services, insurance-related activity, some healthcare and education categories). If you discover this after incorporation, you can end up restructuring or reapplying.

A good practice is to draft a one-page “reality check” before applying: what you sell, where customers are, how you get paid, expected monthly volumes, and which countries are involved. Then validate the license activity against that.

Pitfall 3: Treating UBO and AML as paperwork, not a design constraint

UAE companies typically need to disclose ultimate beneficial ownership (UBO) information and maintain up-to-date corporate records. Even where the registration process is smooth, ongoing compliance expectations remain.

Common issues include:

- Overcomplicated shareholder chains without a clear reason. Multi-layer structures can increase KYC friction, especially for banks.

- Inconsistent story across documents. Deck says “SaaS subscription,” website says “investment,” invoices show “brokerage.” That inconsistency is a compliance red flag.

- Underestimating source of funds and source of wealth questions. This is especially common for holding companies, high-value contracts, or founders moving capital from multiple jurisdictions.

The fix is not “more documents,” it is coherence. Your corporate structure, commercial contracts, and payment flows should tell the same story.

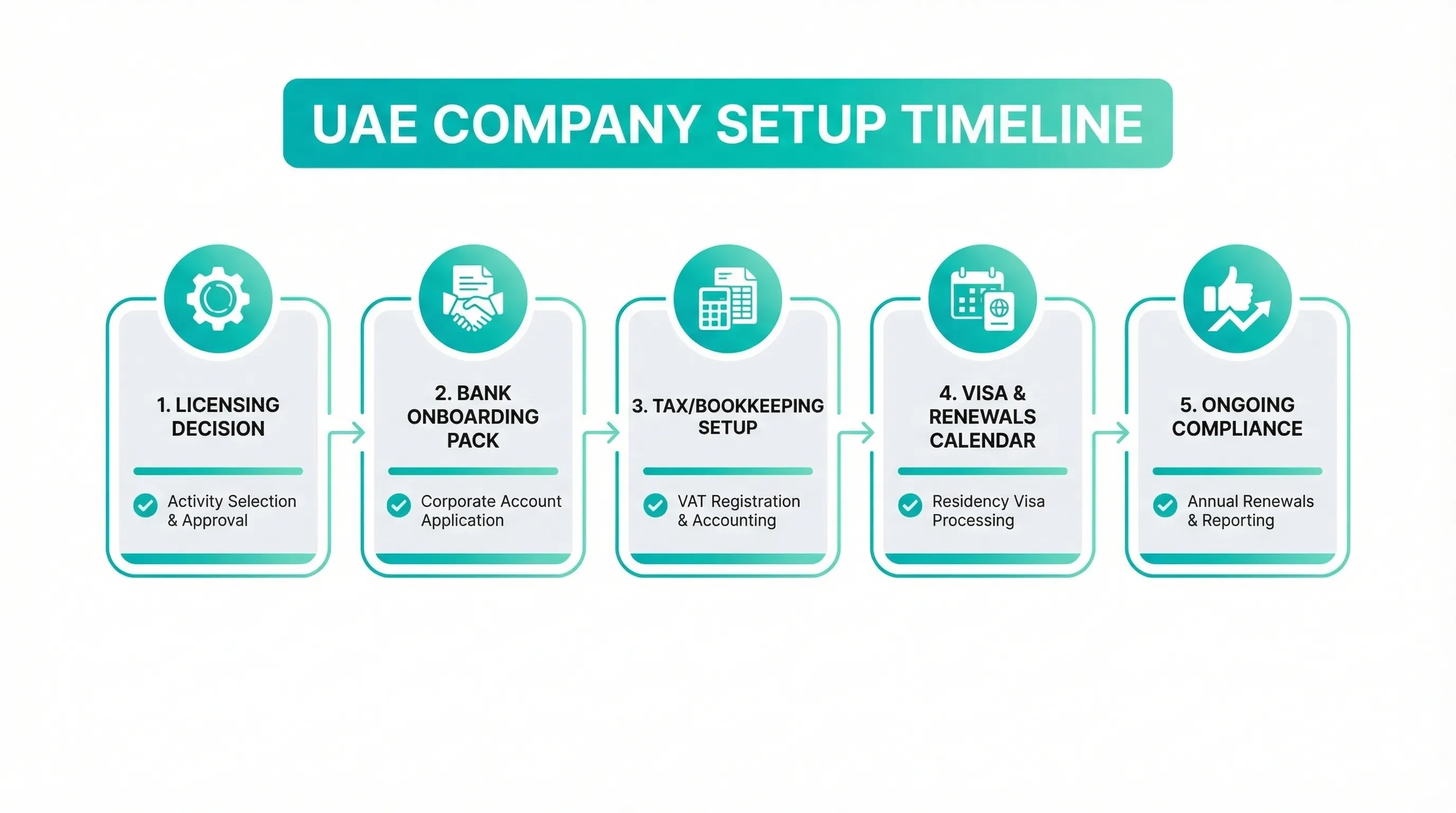

Pitfall 4: Assuming bank account opening is automatic (or quick)

A UAE trade license is not the same as a bankable profile. Account opening timelines vary significantly by:

- activity and risk category

- shareholder residency and nationality mix

- where funds come from and where they go

- quality of the KYC file (and consistency of the narrative)

- whether you can demonstrate real operations (contracts, pipeline, office, employees)

What founders often get wrong is waiting until after incorporation to “figure out banking,” then realizing the chosen setup makes onboarding harder.

What to prepare before you apply to banks

You do not need to over-engineer this, but you should have a clean baseline pack ready:

- a clear business description (products/services, customer locations, expected volumes)

- signed contracts or at least credible proposals and pipeline evidence

- invoices, if already trading elsewhere

- corporate documents (license, MoA, share register as applicable)

- KYC for shareholders and signatories

- a simple flow diagram of money in/out (especially for cross-border models)

If your business involves travel customers, cross-border mobility, or visa-heavy workflows, plan those operational dependencies too. For travel businesses that need an eVisa partner as part of their customer journey, solutions like SimpleVisa’s eVisa platform can reduce administrative friction, but it should be aligned with your licensed activity and compliance narrative.

Pitfall 5: Missing tax and bookkeeping obligations (especially after corporate tax)

The UAE has a modernizing tax environment. Even if your business ultimately qualifies for a favorable outcome (depending on facts and applicable rules), you still need compliant records and timely registrations.

Two frequent mistakes:

- Not setting up bookkeeping from day one. Waiting “until revenue” is how deadlines and filings get missed.

- Assuming zero tax means zero compliance. Even where no tax is due, corporate tax and VAT regimes focus heavily on documentation and correct treatment.

For official guidance, use the Federal Tax Authority resources for UAE Corporate Tax and VAT. (Eligibility and obligations depend on your specific facts, so treat these as starting points, not a substitute for advice.)

What this means in practice

- Decide early who owns bookkeeping: in-house vs outsourced.

- Define your chart of accounts, invoicing format, and document retention.

- Align contracts with how revenue is recognized.

- Do not ignore cross-border VAT questions if you sell services internationally or import goods.

Pitfall 6: Underplanning residency visas, quotas, and renewals

Founders often budget for “a visa,” but immigration planning is more than a one-time application.

Common pitfalls include:

- Assuming visas are unlimited. Some setups tie visas to office type/size or other criteria.

- Not planning dependent visas. Family sponsorship has its own documentation and timing.

- Missing renewal cycles. Trade license renewal, establishment card (where applicable), visas, Emirates ID, medical tests, and tenancy can be interdependent.

A good setup plan includes a calendar of renewal dates and a clear “who does what” internally.

Pitfall 7: Weak governance and signatory controls

This one is less visible at the setup stage, but it causes serious operational risk later.

Typical mistakes:

- issuing broad powers of attorney without limits

- unclear signing authority (who can bind the company and for what)

- no internal approval process for payments and contracts

- using nominee arrangements without understanding responsibilities, liabilities, and documentation standards

Governance does not need to be heavy. Even a simple set of board resolutions, signing policies, and document templates can prevent disputes and banking issues later.

Pitfall 8: Falling for “low price” setups that hide recurring costs

Transparent pricing matters because UAE company management is not a single transaction. Typical recurring or follow-on costs can include:

- license renewals

- office/desk renewals (where applicable)

- immigration renewals and government fees

- bookkeeping, audit requirements (depending on jurisdiction and rules)

- corporate amendments (activities, shareholders, signatories)

A realistic budget should model year 1 and year 2, not only the incorporation invoice.

A practical pre-incorporation checklist (to avoid rework)

Before you submit an application, validate these items in one working session:

- Your top 3 revenue streams and how they map to license activities

- Customer locations (UAE onshore vs international) and contracting needs

- Expected monthly incoming and outgoing payments, currencies, and countries

- Shareholder and UBO structure, kept as simple as possible

- Banking plan (which banks, what KYC story, what proof you have)

- Bookkeeping owner and tax registration timeline

- Visa plan for founders and first hires, plus renewals calendar

If any of these are unclear, it is usually cheaper to pause and design properly than to incorporate quickly and then amend.

Where expert-led structuring makes the biggest difference

The most avoidable pitfalls tend to come from treating company formation as a commodity purchase. In reality, you are engineering a compliant operating system that must satisfy regulators, banks, and commercial counterparties.

Alldren’s positioning, expert-led structuring with transparent, upfront pricing and direct access to senior specialists, is designed for exactly this stage: getting the structure right early, then keeping it compliant as the business grows.

Frequently Asked Questions

What is the biggest mistake when establishing a company in the UAE? The most common mistake is choosing the jurisdiction and license activity before clarifying how the business will operate (where customers are, how revenue is earned, and what banks will accept).

Is a UAE trade license enough to open a bank account? Not always. Banks assess the full risk profile (activity, ownership, expected transactions, documentation quality, and substance). Preparing a coherent KYC pack and business narrative is critical.

Do I need bookkeeping if my company is not making revenue yet? You should set up bookkeeping from day one, even with low activity. Clean records and document retention prevent compliance issues later and simplify tax registrations and filings.

Can I change my license activities later? Often yes, but amendments can take time, cost money, and may trigger additional approvals. It is better to validate activities upfront to avoid operational disruption.

How do I avoid visa and renewal problems? Build a renewals calendar that includes license renewal, immigration steps, and tenancy-related items, then assign an internal owner (or a corporate services partner) to manage deadlines.

Set up once, operate smoothly

If you are establishing a company in the UAE and want to avoid licensing mismatches, banking delays, and compliance surprises, consider getting the structure designed before incorporation. Explore Alldren’s approach at alldren.com to align your setup, governance, and ongoing compliance with how your business actually runs.