Choosing a corporate services provider in the UAE is not just a purchasing decision, it is a risk decision. The firm you appoint will often touch your licensing, compliance calendar, shareholder documentation, banking readiness, tax registrations, and sometimes even immigration and nominee arrangements. If anything in that chain is unclear, you can lose weeks to rework, trigger avoidable compliance exposure, or end up paying for “surprises” that were never scoped.

This guide gives you a practical set of questions to ask before you sign, plus what to look for in the answers. It is written for founders, CFOs, family offices, and international business owners who want a clean UAE setup and reliable ongoing administration.

Why your choice of provider matters more in the UAE than in many jurisdictions

In many countries, company incorporation is relatively standardized, and switching providers later is mostly administrative. In the UAE, the quality of your provider can affect outcomes that are harder to “fix later,” for example:

- Banking readiness: business bank account opening depends heavily on documentation quality, activity clarity, source of funds evidence, and how consistently your profile is presented.

- Regulatory coordination: mainland vs free zone requirements, registrar expectations, and ongoing filings can differ materially.

- Tax and reporting: corporate tax and VAT considerations can influence structuring, timelines, and what you need to prepare from day one. See the UAE Federal Tax Authority’s corporate tax resources for the official baseline requirements (FTA).

- Beneficial ownership and AML/KYC: “company service providers” commonly have AML/CFT obligations and must collect and maintain client due diligence. For context, the UAE Ministry of Economy publishes guidance for DNFBPs (which includes company service providers) (Ministry of Economy).

The point is simple: you are not buying paperwork, you are buying an operating system for your UAE entity.

Do this before you start provider calls (it makes quotes comparable)

Providers often quote based on partial information, then adjust later when realities emerge. To avoid apples-to-oranges proposals, define your “setup profile” up front.

Clarify these items internally (even if you are not 100 percent sure yet):

- Intended activities (as specifically as you can describe them)

- Expected counterparties (countries, types of customers, B2B vs B2C)

- Ownership structure (individuals, corporate shareholders, trusts, holding companies)

- Whether you need UAE residency visas, and roughly how many

- Whether you expect to invoice from the UAE entity, and in which currencies

- Whether you anticipate needing nominee services (only if there is a clear legal and commercial rationale)

You will get better answers when you can ask targeted questions like, “Given this activity and ownership, which jurisdictions are realistic, and what will banking and compliance look like?”

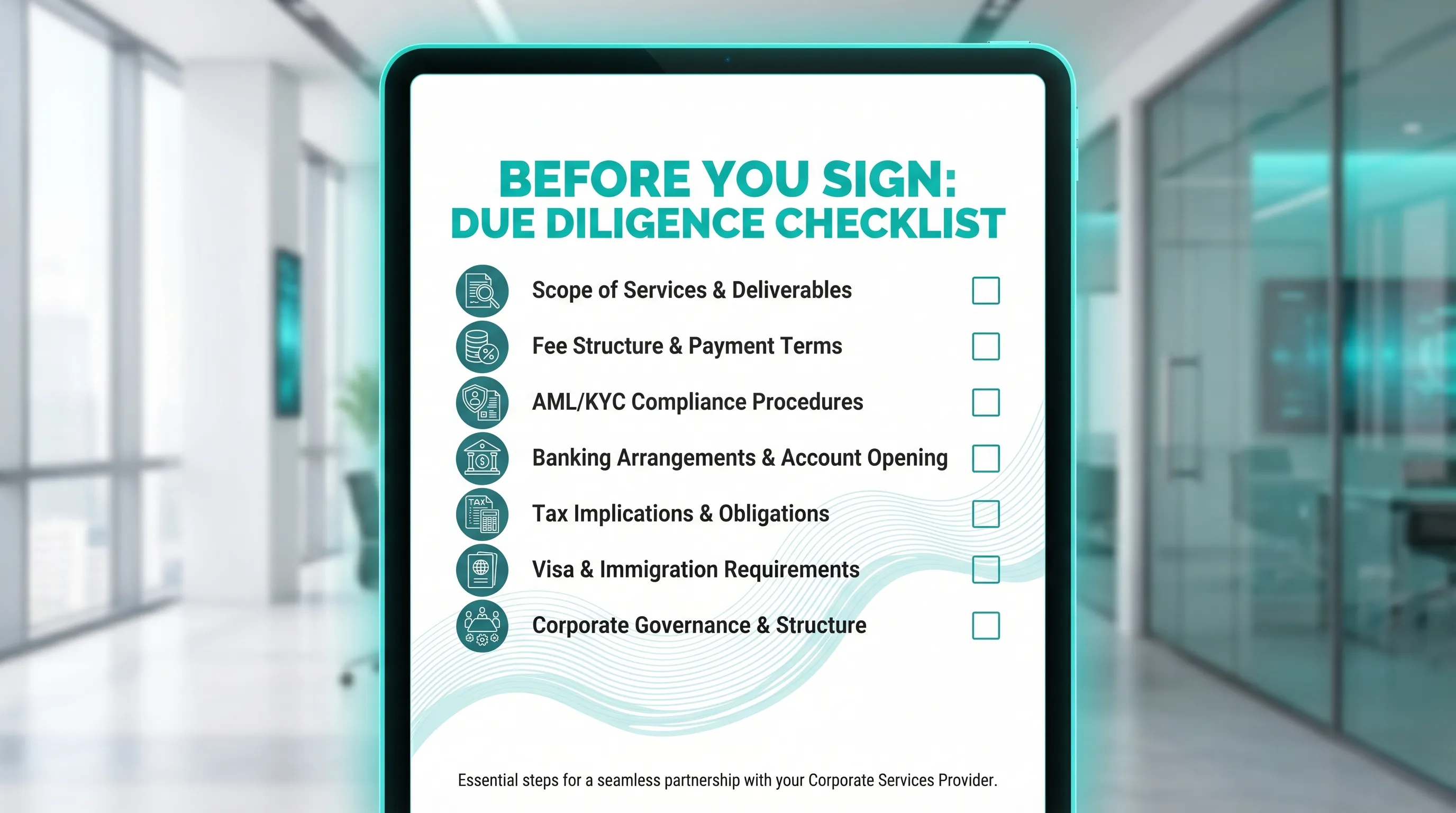

The questions to ask a corporate services provider (and what good answers sound like)

Below are the due diligence questions that tend to surface the real differences between providers.

1) “Who will actually do the work, and who is accountable?”

A common failure mode is a strong sales call followed by execution handled entirely by junior staff, with limited oversight.

What to ask:

- Who is the day-to-day point of contact?

- Who is the senior reviewer or engagement lead?

- If something goes wrong (missed filing, rejected application), who owns resolution?

What a strong answer includes: clear names/roles, escalation paths, and realistic service boundaries.

2) “What exactly is included in the setup scope, and what is excluded?”

Incorporation quotes can hide exclusions like name reservations, additional approvals, establishment card steps, immigration file setup, or document attestations.

Ask for deliverables, not broad promises.

What to ask:

- What are the concrete deliverables (license, incorporation certificate, shareholder registers, resolutions, UBO filing support where applicable, etc.)?

- What is not included, and what commonly triggers additional fees?

- What assumptions is the quote based on (number of shareholders, number of activities, visa count, office type)?

What a strong answer includes: a written scope with assumptions and a change-control approach.

3) “How does pricing work, and how do you prevent surprise fees?”

The best signal of transparency is whether the provider can explain pricing mechanics clearly.

What to ask:

- Is pricing fixed-fee, time-based, or a blend?

- Which third-party fees are pass-through, and are they estimated or confirmed?

- How do you handle scope changes, and how are they approved?

What a strong answer includes: upfront pricing that separates government fees from provider fees, and written approval before extra charges.

4) “What is the realistic timeline, and what are the dependencies on me?”

In the UAE, delays often come from client-side documents (notarization, legalization, KYC evidence), bank compliance questions, or activity-specific approvals.

What to ask:

- What is the best-case and typical timeline for licensing and post-license steps?

- What do you need from me, by when?

- What are the most common reasons your timelines slip?

What a strong answer includes: a dependency list (documents, signatories, KYC items) and timeline ranges rather than guarantees.

5) “How do you handle AML/KYC and source of funds checks?”

If a provider is casual about AML/KYC, that is a red flag, not a convenience. Weak KYC can later harm banking outcomes or trigger re-verification.

What to ask:

- What KYC documents do you require and why?

- How do you assess source of funds and source of wealth?

- How do you store sensitive documents, and who can access them?

What a strong answer includes: a structured onboarding checklist, secure document handling, and clear explanations aligned with UAE AML expectations.

6) “How will you support corporate tax, VAT, and bookkeeping decisions?”

Even if you outsource bookkeeping elsewhere, your provider should be able to explain what decisions matter early and when you must involve a tax professional.

What to ask:

- Do you support corporate tax registration and ongoing compliance administration (where required)?

- Will you advise on whether VAT registration might be relevant, based on my planned turnover and supplies (without over-promising outcomes)?

- How do you coordinate bookkeeping, financial statements, and registrar requirements?

What a strong answer includes: an understanding of boundaries (what is admin support vs tax advice), plus practical planning steps and a compliance calendar.

7) “How do you approach bank account opening, and what will you not promise?”

Banking is often where exaggerated marketing shows up. No credible corporate services provider should guarantee approvals, because banks make independent risk decisions.

What to ask:

- Which banks are realistic for my profile, and why?

- What documentation pack will you help prepare (business plan, contracts, invoices, website, source-of-funds narrative)?

- What does ‘support’ mean in practice: introductions, document preparation, meeting prep, follow-ups?

What a strong answer includes: realistic positioning, a banking readiness checklist, and clarity that outcomes depend on bank compliance.

8) “If I need UAE residency visas, what is the full path and the ongoing obligations?”

Visa processing is multi-step and depends on jurisdiction, quotas, and ongoing renewals. It also intersects with corporate substance and practical operations.

What to ask:

- Which visas are feasible under the chosen structure, and what are the steps?

- What are the estimated time ranges and dependencies (medical, biometrics, Emirates ID)?

- What renewals and compliance actions should I plan for annually?

What a strong answer includes: a step-by-step process map and a renewal plan.

9) “What governance documents and registers will you maintain for me?”

Good governance reduces friction with banks, auditors, counterparties, and regulators. It also makes future restructuring or exit much easier.

What to ask:

- Will you prepare and maintain shareholder resolutions, director resolutions, and statutory registers (as applicable)?

- How do you handle signatory updates, POAs, and changes in shareholders?

- How do you document beneficial ownership changes and reporting obligations?

What a strong answer includes: clarity on what is maintained, where it is stored, and how updates are requested and logged.

10) “If nominee services are involved, what safeguards and legal boundaries apply?”

Nominee arrangements can be legitimate in specific contexts, but they require careful documentation, clear authority boundaries, and risk controls.

What to ask:

- What is the legal structure of the nominee arrangement, and what documents govern it?

- What decisions can and cannot be made by the nominee?

- How do you ensure transparency, reporting, and proper authorization?

What a strong answer includes: a cautious approach, documented approvals, and strong compliance alignment.

A quick comparison table you can use on calls

Use the table below as a live scorecard while you interview providers.

| Question area | Why it matters | What a good answer includes |

|---|---|---|

| Scope and deliverables | Prevents missing steps and add-on fees | Written deliverables, assumptions, exclusions |

| Pricing model | Controls budget and change requests | Split of government vs service fees, approval for extras |

| AML/KYC process | Affects banking and regulatory exposure | Structured checklist, secure storage, clear rationale |

| Tax and bookkeeping coordination | Avoids “setup now, fix later” costs | Compliance calendar, boundaries, referrals when needed |

| Banking support | Sets realistic expectations | No guarantees, readiness pack, practical support steps |

| Visa support | Impacts timelines and operations | Process map, renewal plan, dependencies |

| Governance and registers | Reduces future friction | Document control, update workflow |

| Account management | Determines execution quality | Named owner, escalation path, response times |

Green flags and red flags when choosing a provider

A few patterns show up repeatedly in successful UAE setups.

Green flags:

- The provider asks detailed questions about your activity, counterparties, and ownership before recommending a structure.

- They separate what is certain (process, required documents, known fees) from what is not (bank outcomes, third-party timing).

- They provide a written scope with assumptions and explain change control.

- You have direct access to a senior expert for complex structuring and risk decisions.

Red flags:

- Guaranteed bank account approval, guaranteed timelines, or “no documents needed” messaging.

- Vague “all-in” quotes that do not separate government fees and service fees.

- Minimal AML/KYC checks, or reluctance to explain how your data is stored.

- Pressure to pick a jurisdiction before understanding your activity and compliance needs.

What to request in writing before you sign

Verbal reassurance does not help when you are mid-process and a document is rejected or an approval is delayed. Ask for written clarity.

Request these items:

- A proposal or scope of work listing deliverables, exclusions, assumptions, and timelines

- A fee schedule separating government fees from service fees, plus payment milestones

- A list of documents you must provide, including any notarization or legalization requirements

- Your ongoing compliance calendar (license renewal, filings, bookkeeping cadence, tax registrations where applicable)

- The engagement terms, including who your responsible lead is and how escalation works

Frequently Asked Questions

What does a corporate services provider do in the UAE? A corporate services provider can support UAE company setup and structuring, licensing administration, ongoing compliance, governance, banking support, and often visas and related corporate services, depending on the engagement.

Should a corporate services provider guarantee a UAE bank account? No. Banks make independent compliance decisions, and outcomes depend on your profile, activity, documentation, and bank risk appetite. A good provider should prepare you and improve readiness, not promise approvals.

How do I compare quotes from different corporate services providers? Compare written scope and assumptions first, then compare fees. Low quotes often exclude steps like attestations, amendments, additional approvals, or post-license administration.

What are common hidden costs in UAE company setup? Common surprises include extra government approvals tied to activities, document attestation/legalization, amendments for shareholder changes, and additional compliance work triggered by incomplete KYC documentation.

Do I need ongoing compliance support after incorporation? In most cases, yes. Even simple structures have renewal cycles, governance upkeep, and increasing expectations around documentation quality for banking, tax, and counterparties.

Need an expert-led, transparent UAE setup?

If you want a corporate services provider that prioritizes clear scope, upfront pricing, and direct access to senior expertise for structuring and compliance decisions, explore how Alldren supports UAE company setup, ongoing compliance management, governance, banking support, and residency visa processing. Share your objectives and constraints, and get a clear plan before you commit.