Corporate tax is now a standard part of doing business in the UAE, and corporate tax registration is the first compliance step that determines how you interact with the Federal Tax Authority (FTA), from receiving your Corporate Tax Registration Number (CT TRN) to filing returns.

If you are a mainland LLC, a free zone entity, a branch, a holding company, or even a self-employed individual meeting the conditions, registration is not optional. The practical challenge is that the UAE corporate tax regime has clear rules, but real-life cases (multiple licenses, groups, free zone activities, mixed income) can make the filing process feel less straightforward.

This guide explains who must register, what you need before you start, how to file through the FTA portal, and what to do after you get your CT TRN.

What corporate tax registration is (and what it is not)

Corporate tax registration is the process of registering a taxable person (or a person required to register) with the FTA for UAE Corporate Tax, which results in the issuance of a Corporate Tax Registration Number (CT TRN).

It is not the same as:

- VAT registration: VAT and Corporate Tax are separate regimes. You can be VAT-registered and still need to register for Corporate Tax (and vice versa).

- Economic Substance Regulations (ESR) filings: ESR requirements have changed over time and are separate from Corporate Tax obligations.

- License issuance/renewal: Your trade license does not automatically register you for Corporate Tax.

For the official framework and updates, refer to the UAE Ministry of Finance corporate tax hub and FTA guidance: UAE Ministry of Finance Corporate Tax and Federal Tax Authority Corporate Tax.

Who must register for UAE Corporate Tax

In UAE Corporate Tax, the registration obligation depends on whether you are a juridical person (company or legal entity) or a natural person (individual conducting business), and on your UAE nexus (residency, incorporation, or permanent establishment).

Juridical persons (companies and other legal entities)

You will generally need corporate tax registration if you are any of the following:

- A UAE incorporated entity, including mainland companies and most free zone entities.

- A foreign entity that is effectively managed and controlled in the UAE (treated as a UAE tax resident under the rules).

- A non-resident with a permanent establishment in the UAE, or otherwise deriving UAE-sourced income where registration applies.

Important nuance for free zones:

- Many free zone entities still need to register and file, even if they expect to be taxed at 0% as a Qualifying Free Zone Person (QFZP) on qualifying income.

- “0%” is not the same as “not in scope.” The compliance expectations (registration, filings, substance, transfer pricing where relevant) can still apply.

Natural persons (individuals doing business)

Individuals can also have corporate tax obligations when they conduct a business or business activity and meet the conditions set out in the corporate tax framework (for example, where turnover thresholds apply for business income).

This commonly affects:

- Freelancers and sole proprietors operating under a license.

- Individuals with multiple business activities under their name.

- Professionals who invoice clients directly and meet the criteria to be treated as conducting a business.

If you are unsure whether your income is business income for corporate tax purposes, the safest approach is to validate your classification before filing, because misclassification can lead to late registration risk.

Key timelines to know before you file

Two timelines matter most for compliance planning:

- Registration deadline: The UAE has issued specific registration deadlines through FTA decisions that can vary based on factors such as the type of person (juridical vs natural) and license-related details. Do not guess your deadline, confirm it against the latest FTA decision and your entity profile.

- Return filing and payment deadline: The corporate tax return is generally due within 9 months after the end of the relevant tax period, along with payment of tax due (if any).

Here is a practical overview of what to track.

| Compliance item | What it affects | Typical rule of thumb | Where to confirm |

|---|---|---|---|

| Corporate tax registration deadline | Late registration penalties, compliance status | Deadline depends on FTA decision criteria and your profile | FTA announcements and decisions on tax.gov.ae |

| Tax period (financial year) | Determines first return timing | Often aligned to financial statements, but can vary | Your constitutional documents and accounting basis, plus FTA rules |

| Corporate tax return filing | Filing obligation even if tax is 0 in some cases | Generally within 9 months after tax period end | FTA corporate tax guidance |

| Record keeping | Audit readiness and defensibility | Keep accounting and supporting records for required statutory period | FTA guidance and applicable laws |

If you are setting up a new entity, it is worth aligning the tax period, accounting processes, and governance from day one. Fixing these after registration is possible, but it is rarely efficient.

What you need to prepare for corporate tax registration

The EmaraTax registration flow is easier when you have the right information ready. In practice, delays often come from mismatched license details, unclear ownership information, or missing identification documents for authorized signatories.

Core details you will likely need

While exact fields can change as the FTA updates the portal, most applicants should expect to provide:

| Information area | Examples of what may be requested | Common pitfalls |

|---|---|---|

| Entity identification | Legal name (English and Arabic if applicable), legal form, license number, issuing authority | Using a commercial name that does not match the license |

| Registration and addresses | Registered address, business activity location, contact details | Inconsistent addresses across documents |

| Ownership and control | Shareholders/partners, ownership percentages, beneficial owner details where applicable | Missing shareholders in complex structures |

| Authorized signatory | Person authorized to act on behalf of the entity, ID details | Signatory not properly authorized or documentation unclear |

| Tax period and accounting | Financial year start and end, accounting standards used | Choosing dates that conflict with audited statements or group policies |

| Group and relationships | Tax group intention, related parties | Not flagging group structures early, leading to rework later |

Before you start, sanity-check these items

- Your trade license details match exactly what you will enter.

- Your ownership structure is clearly documented, especially if there are multiple layers or overseas holding entities.

- Your financial year is confirmed (and consistent with accounting and governance decisions).

- You know whether you are likely to claim any specific treatment (for example, free zone qualifying treatment, tax grouping, or small business relief where applicable).

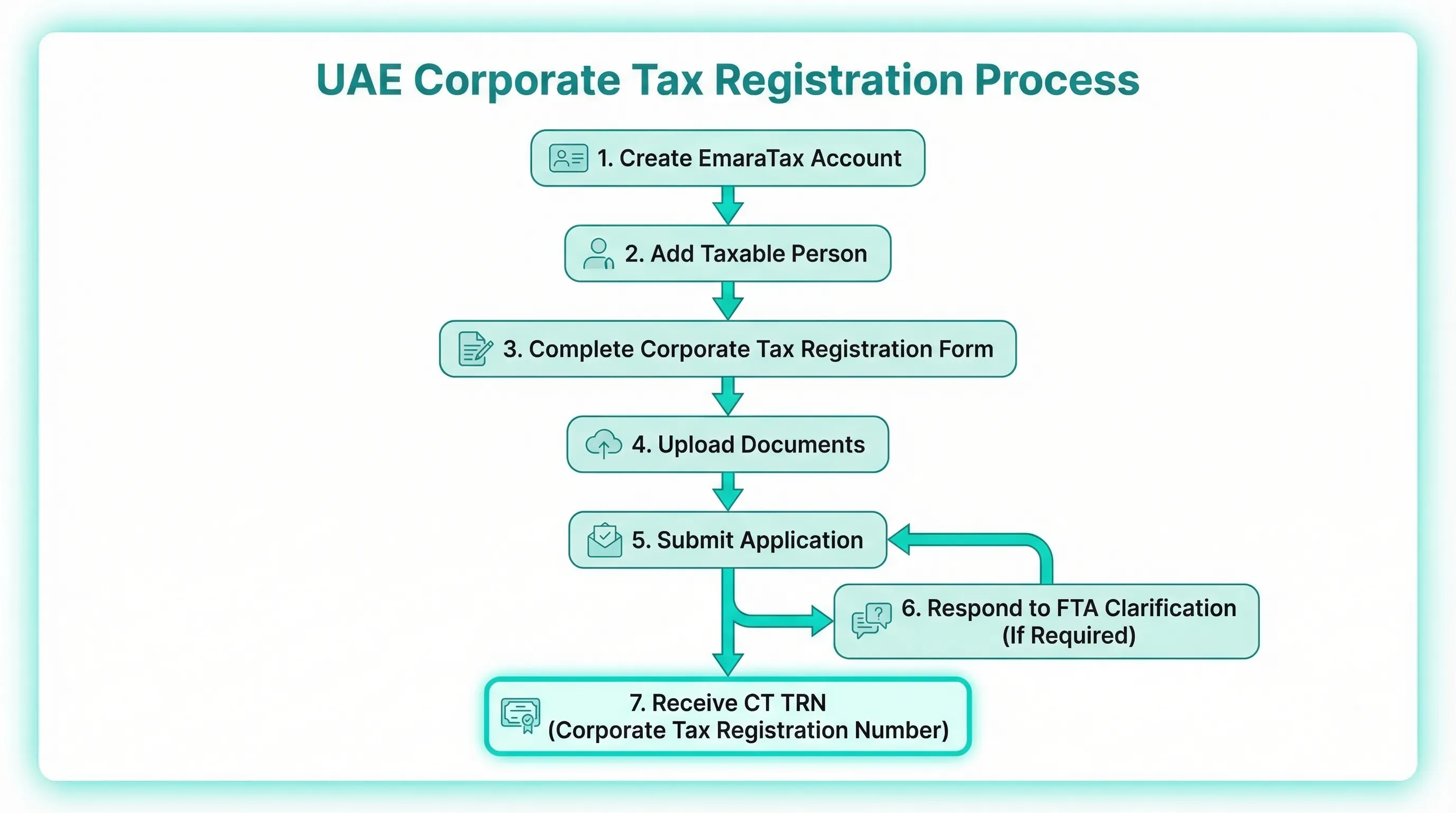

How to file corporate tax registration in the UAE (step-by-step)

Corporate tax registration is typically completed online through the FTA’s digital platform (EmaraTax). The screens and labels can evolve, but the workflow usually follows the same logic.

1) Access EmaraTax and your taxable person profile

- Log in to the FTA portal (EmaraTax) via tax.gov.ae.

- Confirm you are operating under the correct user credentials and that you can see the correct entity profile (or create/add it if needed).

If you are already VAT-registered, you may see the entity under your existing profile, but corporate tax registration still requires completing the corporate tax section.

2) Start the Corporate Tax registration application

Within the portal:

- Choose the option to register for Corporate Tax.

- Confirm the applicant type (juridical person or natural person).

Be careful here. Selecting the wrong person type can cause unnecessary back-and-forth and delays.

3) Enter entity and license information

Typical inputs include:

- Legal name and legal form

- License number, license issue details, and licensing authority

- Business activities

- Registered and operational addresses

Tip: Enter details exactly as shown on your license and constitutional documents. “Close enough” can trigger clarification requests.

4) Add ownership, management, and authorized signatory details

You will typically declare:

- Shareholders and ownership percentages

- Management and control information (depending on the entity)

- The authorized signatory acting with the FTA

If your structure is complex (multiple entities, trusts, nominee arrangements, cross-border ownership), it is worth validating what should be disclosed and how it aligns with your broader compliance framework.

5) Confirm tax period and relevant corporate tax positions

You may be asked for:

- Financial year start and end

- Whether the entity is part of a group or intends to form a tax group

- Whether the entity is a free zone person (and related declarations)

This step is where many businesses accidentally create downstream issues. For example, free zone entities may assume the portal selection equals automatic 0% treatment. In reality, the 0% outcome depends on meeting the conditions and maintaining compliance.

6) Upload supporting documents (as requested)

Upload the documents the portal requests for your case. Requirements can vary based on the entity type and what you declare.

Focus on legibility and consistency. A surprising number of registration delays come from:

- Unclear scans

- Expired IDs

- Mismatched names (spacing, spelling differences)

7) Submit and monitor for clarification requests

After submission:

- Track your application status inside the portal.

- Respond quickly to FTA clarification requests.

Once approved, you will receive your Corporate Tax Registration Number (CT TRN).

What happens after you receive your CT TRN

Registration is not the finish line. It is the point where corporate tax compliance becomes operational.

Maintain accurate records from the start of your first tax period

Corporate tax is built on financial results and tax adjustments. If your bookkeeping is inconsistent, the return becomes a reconstruction exercise.

At a minimum, ensure you can support:

- Revenue recognition

- Expense substantiation (invoices, contracts, proofs of payment)

- Related party transactions and pricing logic (where applicable)

- Fixed asset schedules and depreciation policies

If you need help setting up compliant bookkeeping and tax-ready processes, this is exactly where many businesses use a corporate services partner to avoid preventable errors.

Plan for your corporate tax return filing

Even if you expect 0% corporate tax (for example, due to small taxable income, reliefs, or free zone qualifying treatment), you may still have a filing requirement.

Return filing typically includes:

- Declaring taxable income calculations

- Confirming elections and treatments

- Paying corporate tax due (if applicable)

Keep your FTA profile updated

If any key details change, for example, license changes, address changes, ownership updates, you should review whether the FTA portal details must be updated to avoid compliance misalignment.

Common corporate tax registration mistakes (and how to avoid them)

Mistake 1: Assuming you are exempt because you are in a free zone

Free zone status can change the tax outcome, but it does not automatically remove obligations.

Avoid it by:

- Confirming whether you are a free zone person, and whether you expect to be a Qualifying Free Zone Person.

- Ensuring your operating model matches the conditions needed for your intended treatment.

Mistake 2: Waiting until the deadline without checking what your deadline is

The UAE corporate tax registration deadlines are not a single universal date for everyone.

Avoid it by:

- Identifying your applicable deadline early using the latest FTA decisions and guidance.

- Building in time for clarifications and document corrections.

Mistake 3: Mismatched legal names and license information

A small mismatch can trigger clarifications.

Avoid it by:

- Copying details directly from the trade license and constitutional documents.

- Keeping a single “source of truth” file for entity details used across banks, licensing, VAT, and corporate tax.

Mistake 4: Registering the wrong person (entity vs individual)

In some cases, business is conducted through a company. In other cases, an individual conducts the business directly.

Avoid it by:

- Confirming the contracting party on invoices and contracts.

- Confirming who holds the license and who earns the income.

Mistake 5: Not aligning registration with your accounting setup

Corporate tax compliance depends on the quality of your books.

Avoid it by:

- Setting up bookkeeping and a chart of accounts that can support tax reporting from day one.

- Tracking related party transactions properly if you have multiple entities.

Penalties and compliance risk: why timing matters

The FTA can impose administrative penalties for non-compliance, including late registration and late filing. Penalty rules can be updated through Cabinet decisions and FTA guidance, so treat penalty amounts and triggers as something you should confirm against current official sources.

The business risk is not only the penalty itself. Late registration can also create:

- Complications in bank and compliance processes

- Backlog pressure when you need clean records retroactively

- Increased audit risk if filings and records are not consistent

If you are uncertain about your required timeline, confirm it early. Doing so is almost always cheaper than fixing a late registration situation.

When it makes sense to get professional support

Corporate tax registration is often simple for a single-license, single-owner business with clean documents. It becomes more sensitive when you have any of the following:

- A free zone structure with mainland customers or mixed activities

- Multiple licenses or branches

- Cross-border ownership or management and control questions

- Plans for tax grouping

- Related party transactions that should be tracked correctly from the start

Alldren supports UAE businesses with corporate structuring, compliance, and ongoing corporate services. If you want a senior-led review before you submit, or you want someone to manage the end-to-end compliance workflow (registration through filing readiness), you can explore Alldren’s corporate services at alldren.com.

A practical checklist before you click “Submit”

Before you submit your corporate tax registration application, confirm:

- Your entity name, license number, and licensing authority match the trade license exactly.

- Your authorized signatory documentation is clear and current.

- Ownership details are complete and consistent with your corporate records.

- Your financial year dates are correct and aligned with your accounting.

- You have a plan for bookkeeping quality and return readiness, not only registration.

Done right, corporate tax registration in the UAE becomes a clean administrative step that sets up everything that follows: accurate filings, lower compliance risk, and a structure that can scale with your business.