Most UAE companies fail financially for boring reasons, not dramatic ones: weak documentation, messy books, delayed tax registrations, and bank compliance issues that quietly choke cash flow. The fix is rarely “more accounting”. It is building the right business finance services stack early, so banking, tax, and reporting all reinforce each other.

This guide breaks down the finance services that commonly become non-negotiable for UAE businesses (from first invoice through scale), what triggers each one, and what “good” looks like in 2026.

What “business finance services” really means in the UAE

In many countries, “finance services” is shorthand for bookkeeping and tax filing. In the UAE, it is broader because banking onboarding, licensing, substance expectations, and tax compliance are tightly linked. A “finance stack” typically spans:

- Banking access (account opening, KYB, ongoing bank compliance)

- Accounting and records (IFRS-based financials, reconciliations, audit readiness)

- Tax operations (VAT, corporate tax, registrations, returns, and defensible positions)

- Controls and governance (approvals, related-party discipline, documentation)

- Cash management (forecasting, budgeting, FX planning)

If you operate across mainland and free zones, or run multiple entities (holding company, operating company, SPVs), the need for consistent processes becomes even more important.

Business finance services every UAE company may need (and when)

Not every company needs every service on day one, but most businesses end up needing some version of the following.

1) Corporate bank account opening support (and banking hygiene)

For many founders, the real “start” of operations is when the business can bank, receive client funds, and pay suppliers. In 2026, account approval is still heavily driven by documentation quality and operational substance.

Common support areas include:

- Selecting the right bank tier for your activity and profile

- Preparing KYB packs (corporate documents, UBO details, contracts, invoices, source of funds)

- Designing a clean transaction narrative from day one (so your statement makes sense)

- Ensuring your office and presence evidence aligns with current expectations

If you have relied on generic virtual office solutions, it is worth understanding how banks evaluate address and “physical nexus” signals now. Alldren covered this in detail in When a Flexi-Desk Is Not Enough: UAE Corporate Banking Address Requirements in 2026.

Why this counts as a finance service: without banking, invoicing and tax compliance are theoretical. Also, banking friction often forces founders into risky workarounds (personal accounts, third-party payment collection) that later create audit and tax problems.

2) Bookkeeping and financial statements (IFRS-aligned)

Bookkeeping is the foundation for VAT, corporate tax, audits, shareholder reporting, and sometimes even visa or license renewals. The most common failure mode is “bank balance accounting”, where founders treat the bank statement as the ledger.

A robust setup usually includes:

- A fit-for-purpose chart of accounts (designed for your revenue model)

- Monthly bank reconciliations (not quarterly catch-ups)

- Clear expense substantiation (contracts, invoices, receipts, business purpose)

- Proper separation of owner and company transactions (critical for corporate veil discipline)

Even small companies benefit from monthly closes because they reveal:

- Margin drift (pricing vs delivery cost)

- Taxable income direction (before it becomes a surprise)

- Working capital pressure (receivables aging and payable timing)

3) VAT registration, VAT returns, and VAT evidence management

VAT is operationally simple only if your records are clean. Many UAE businesses stumble on VAT because they focus on the rate (often 0 percent on exported services) but underestimate the documentation and classification work.

You typically need VAT finance services when:

- You approach or exceed the mandatory registration threshold

- You export services and need to defend zero-rating with correct evidence

- You issue high volumes of invoices and need structured invoice logic

In 2026, documentation discipline matters even more because invoicing systems and data matching are tightening. For deeper context, see VAT and Global Services: Why Zero-Rated Exports Still Require Registration.

Practical point: a “VAT service” is not only filing. It is also building a repeatable ruleset for place of supply, customer location evidence, and correct invoice fields.

4) Corporate tax registration, tax computation support, and filing readiness

With UAE corporate tax now part of normal operations, businesses need a recurring cycle that turns accounting records into defensible tax positions.

Finance services commonly include:

- Corporate tax registration and ongoing status management

- Provisioning and estimating (so you know where you stand before year-end)

- Treatment of non-deductible expenses and related-party items

- File-ready working papers that match what auditors and tax reviewers expect

If you are a smaller business targeting 0 percent via Small Business Relief, the mechanics and trade-offs matter (including the election timing and the consequences of crossing the revenue threshold). Alldren explains the 2026 position in UAE Small Business Relief in 2026: Securing the 0% Corporate Tax Position.

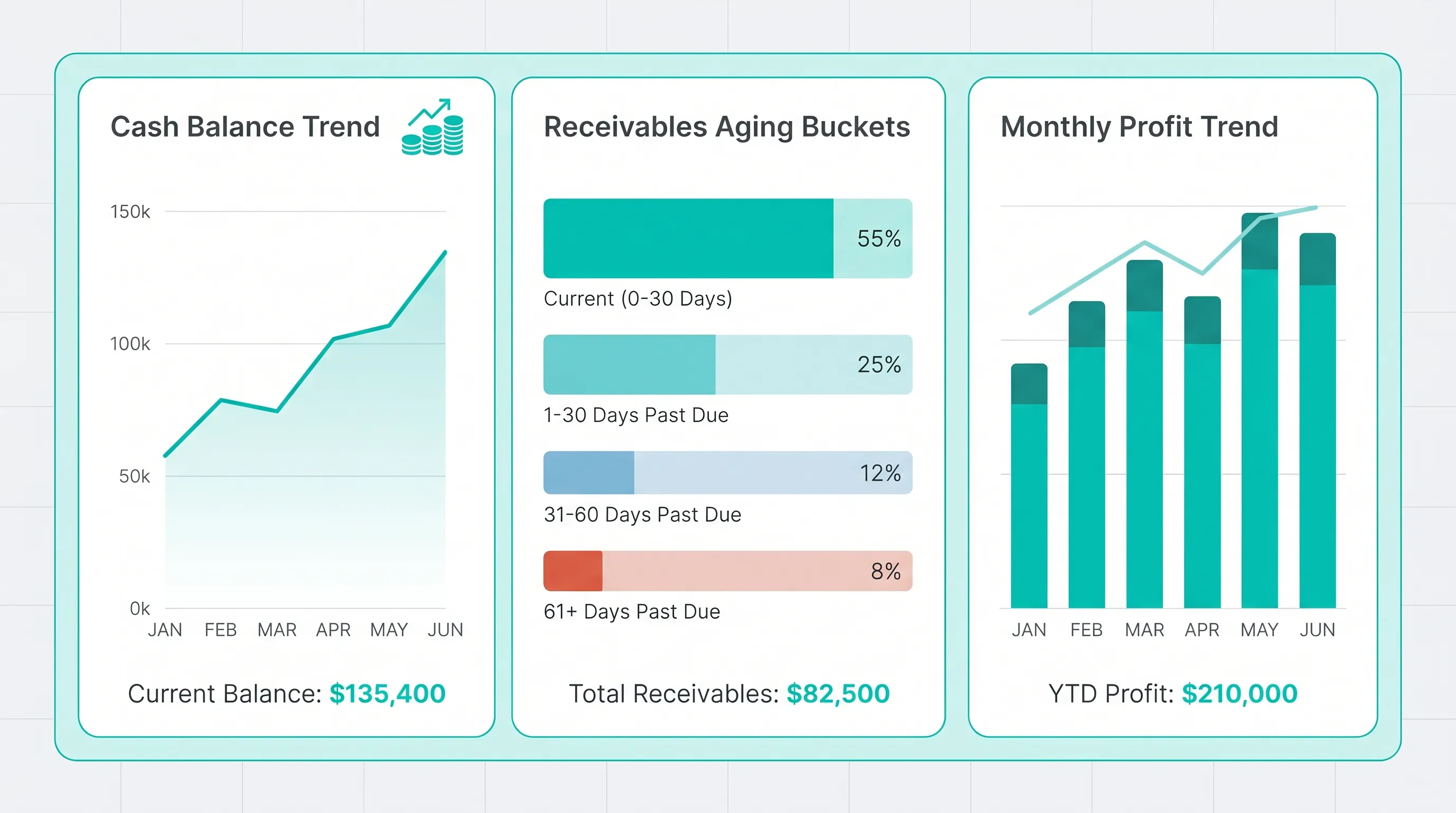

5) Management reporting (for founders, boards, and banks)

Statutory financials tell you what happened. Management reporting helps you decide what to do next.

Even a lean monthly pack can prevent common UAE growth problems (overhiring, VAT cash traps, dependency on one client, and weak collections). Typical components include:

- Profit and loss with margin by service line

- Balance sheet with working capital movement

- Cash flow forecast (next 13 weeks is often enough)

- Receivables aging and collections pipeline

Banks and counterparties also respond well to companies that can produce consistent reporting quickly, especially during periodic compliance reviews.

6) Cash flow forecasting and treasury basics

Many UAE companies are profitable on paper but stressed in cash because of payment terms, retention mechanics, seasonality, or inventory cycles.

Treasury and cash services can be simple but high impact:

- Building a rolling cash forecast tied to real invoices and payables

- Planning VAT and corporate tax cash timing

- Setting approval rules for large payments and owner withdrawals nIf you deal in multiple currencies, even basic FX discipline (quoting policy, conversion timing, and avoiding unnecessary spreads) becomes a material finance function.

7) Payroll operations and employee cost compliance

Payroll is often a founder’s first recurring process with penalties attached. Requirements vary by jurisdiction, employee type, and bank arrangements, so payroll support typically focuses on:

- A clean payroll register that ties to contracts and visa records

- Correct treatment of allowances and reimbursements

- Payment workflows that produce consistent evidence (for audits and banking reviews)

Even if your team is small, payroll is a common “source of truth” used in substance narratives, budgeting, and operational reporting.

8) Audit coordination and audit readiness

Not every UAE entity is audited every year, but many free zones, banks, and counterparties request audited financial statements or audit-like documentation.

Audit readiness services usually include:

- Getting the general ledger and schedules into audit shape (fixed assets, receivables, related parties)

- Preparing supporting documentation folders

- Coordinating with external auditors so the process finishes on time

This becomes particularly important when you need audited accounts for banking, restructuring, investor due diligence, or clean business exits.

9) Finance controls, approvals, and governance documentation

Controls sound “corporate”, but they are often what keeps a growing founder-led business bankable and tax defensible.

Examples of basic controls that matter in the UAE:

- Clear rules on who can sign contracts and approve payments

- Written policies for reimbursements and owner expenses

- Documentation for related-party transactions (especially across group entities)

- Board or manager resolutions for major decisions (bank changes, loans, profit distributions)

Controls also reduce the risk of accidentally creating inconsistencies between what the business does and what it claims in banking or tax narratives.

Quick decision table: which services are triggered by what?

| Business finance service | Common trigger in the UAE | What “good” looks like | What goes wrong if ignored |

|---|---|---|---|

| Bank account opening support | New incorporation, bank upgrade, compliance review | KYB pack prepared, clear business narrative, clean governance | Rejections, frozen onboarding, pressure to use personal accounts |

| Bookkeeping and monthly close | First invoices, recurring expenses, hiring, multi-entity group | Reconciled books monthly, documented expenses, entity separation | VAT and CT errors, weak audit trail, shareholder disputes |

| VAT registration and VAT returns | Threshold reached or expected, export services, mixed supplies | Correct VAT treatment, evidence stored, timely filings | Penalties, denied zero-rating, cash flow surprises |

| Corporate tax compliance | First tax period, revenue growth, group transactions | Clear tax computation support, defensible positions, records ready | Underpayment risk, rework during audits, preventable tax cost |

| Management reporting | Growth, fundraising, bank scrutiny, multiple products | Monthly pack, cash forecast, receivables discipline | Decisions made “blind”, delayed response to cash stress |

| Cash flow forecasting | Long payment terms, seasonal revenue, inventory, tax cycles | 13-week rolling forecast tied to real data | Insolvency risk despite profitability |

| Payroll support | Hiring, visa scaling, bank scrutiny | Payroll register matches contracts and payments | Employee disputes, poor documentation during reviews |

| Audit readiness | Free zone requirement, bank request, investor due diligence | Schedules prepared, supporting docs organized | Missed deadlines, qualified opinions, delayed banking outcomes |

| Controls and governance documentation | Multiple signatories, related parties, fast growth | Written approvals, clean policies, documented decisions | Increased AML/bank scrutiny, tax defensibility weaknesses |

A practical way to build your finance stack (without overbuilding)

A sensible sequencing for many UAE businesses is:

Start-up stage (first 90 days)

Focus on banking + clean books.

- Build a KYB-ready document folder from day one (contracts, invoices, UBO docs)

- Implement bookkeeping with bank reconciliation and a basic chart of accounts

- Decide early whether VAT registration is imminent

Operating stage (consistent revenue)

Add tax operations + reporting.

- Move to monthly closes and management reporting

- Put VAT evidence management on rails (especially for exported services)

- Prepare for corporate tax computations, not only year-end filing

Scale stage (team growth, multi-entity, external capital)

Add controls + audit readiness.

- Formalize approvals, expense policies, and related-party documentation

- Create audit-ready schedules and ensure each entity’s finances are ring-fenced

How Alldren fits in

Alldren provides corporate services for establishing and managing UAE companies, including business and financial services that support compliant, bankable operations. If you need help aligning bookkeeping, VAT, corporate tax, banking, and governance into a single operating system (without guesswork), you can review Alldren’s approach at alldren.com.

Frequently Asked Questions

What are business finance services in the UAE? Business finance services typically include banking support, bookkeeping and financial statements, VAT and corporate tax operations, payroll processes, management reporting, and audit readiness.

Do I need bookkeeping if my UAE company is small? Yes in most cases. Even small companies benefit from reconciled books because VAT, corporate tax, banking reviews, and audits depend on clean underlying records.

If my services are zero-rated, do I still need VAT registration? Often, yes. Zero-rated supplies can still count toward mandatory VAT registration thresholds, and you still need evidence and compliant invoices. Your facts should be reviewed carefully.

What is the biggest finance mistake UAE founders make? Mixing personal and company transactions (or using personal accounts for business) is one of the most damaging mistakes because it creates banking, tax, and audit problems later.

When should I prepare for UAE corporate tax filing? Ideally from your first tax period. Corporate tax readiness is mostly about recordkeeping and classifications across the year, not a last-minute form submission.

Talk to an expert about your UAE finance stack

If you want a finance function that is built to survive bank scrutiny, VAT checks, and corporate tax audits (without consuming founder time), Alldren can help you set up and run the operating backbone: banking support, bookkeeping, tax registrations, compliance management, and governance. Explore your options or speak with a senior specialist at Alldren.