A RAK ICC company can be an efficient vehicle for holding shares, isolating a single transaction, or organizing private assets. The important word is can. The structure works best when the legal wrapper matches the commercial purpose, the banking story is credible, and the compliance file is built from day one.

For founders, investors, family offices, and private clients, the attraction is clear: a UAE registered international company, flexible ownership, no need for a full operating office, and a structure that can sit cleanly in a cross-border plan. But a RAK ICC company is not a universal shortcut. It is not a local UAE trading license, it does not automatically create tax residency in every sense that a bank or foreign tax authority may require, and it should not be used as a substitute for proper asset planning.

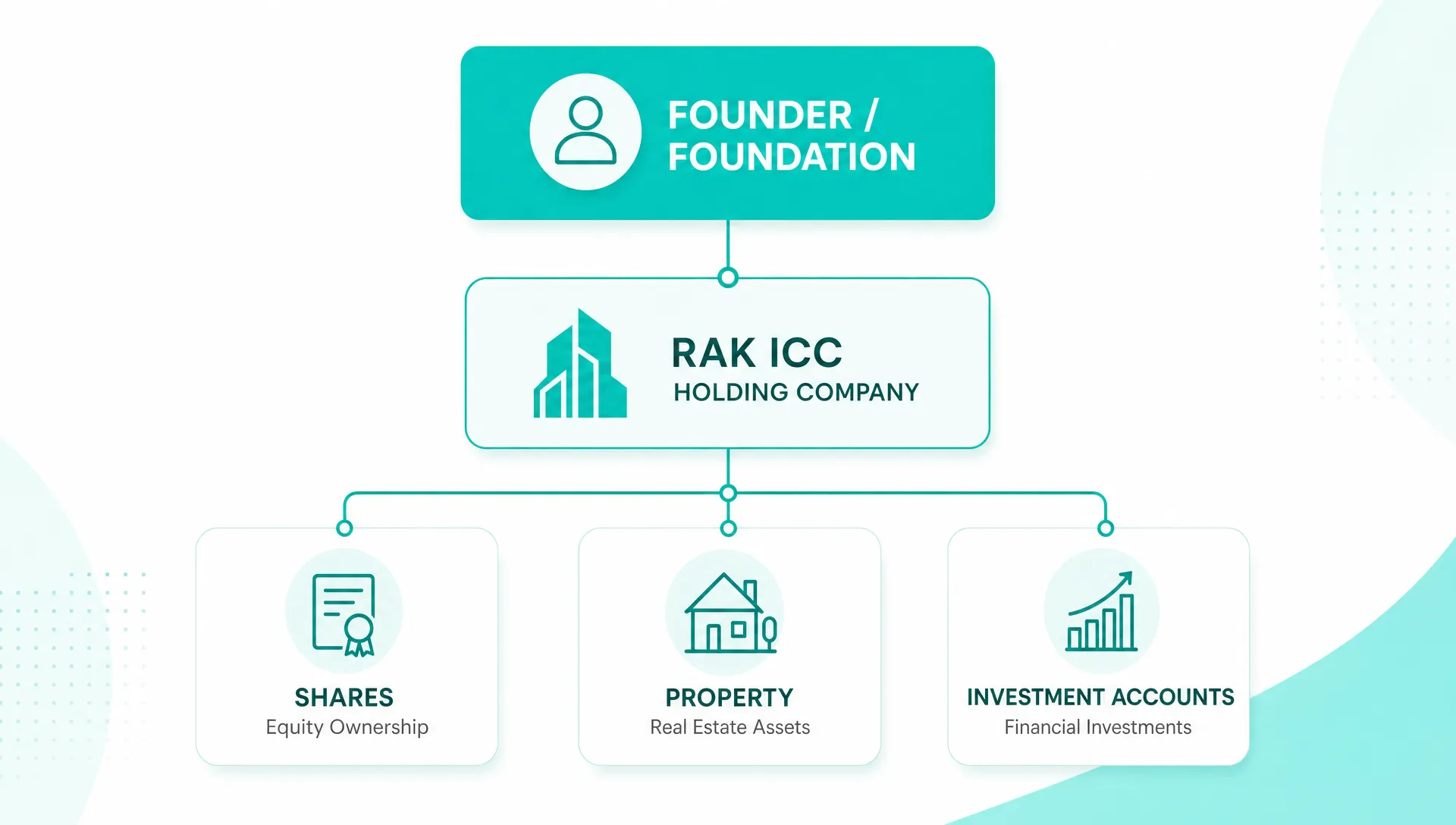

This guide focuses on how to think about RAK ICC for three specific purposes: holding companies, SPVs, and asset plans.

What a RAK ICC company is, and what it is not

RAK ICC stands for Ras Al Khaimah International Corporate Centre, a corporate registry in the Emirate of Ras Al Khaimah. The registry is designed for international business companies and related structures, including certain holding, investment, and special purpose arrangements. You can review the registry framework through the official RAK ICC website, but the practical point is simple: RAK ICC is a corporate platform, not an operating mainland or free zone license for doing local UAE business.

That distinction matters because many planning mistakes start with the word offshore. A RAK ICC company may be incorporated in the UAE, but it is typically used for international or passive purposes rather than UAE onshore operations.

In practical terms, this means:

- It can be useful for holding shares, investment assets, intellectual property, or specific transaction assets.

- It is generally not the right vehicle for hiring staff, renting a commercial office, invoicing UAE customers as a local operating business, or applying directly for UAE residence visas.

- It usually works through an approved registered agent, who helps maintain the company at the registry level.

- It still requires serious compliance, including beneficial ownership information, accounting records, board approvals, tax analysis, and banking documentation.

If you are still comparing whether this type of vehicle is appropriate at all, Alldren has a separate guide on RAK ICC offshore company best uses and limits that covers the broader suitability question.

The three planning use cases: holding, SPV, and asset plan

A RAK ICC company is most effective when it has a narrow, defensible purpose. The same registry can support different outcomes, but the structuring logic changes depending on the goal.

| Use case | Main purpose | Typical assets or activities | Key planning question |

|---|---|---|---|

| Holding company | Centralize ownership | Shares, subsidiaries, investment portfolios, IP, real estate interests where permitted | What should the company own, and how will income or exits flow? |

| SPV | Ring-fence one transaction or liability pool | A property acquisition, joint venture, financing, project asset, or single investment | What risk is being isolated, and who controls the SPV? |

| Asset plan | Organize ownership, succession, and protection | Family wealth, private investments, digital assets, property, operating company shares | Who should own, control, benefit, and inherit? |

These categories overlap. A holding company can also be an SPV if it owns only one asset. An asset plan may include several RAK ICC companies under a foundation or other estate planning vehicle. The right answer depends less on the label and more on the legal and financial flow.

Using a RAK ICC company as a holding company

A holding company plan starts with a basic question: what needs to be held, and why should it be held through a UAE international company rather than directly by an individual or another entity?

Common reasons include consolidating shareholdings, simplifying future transfers, separating personal assets from business assets, supporting a sale or investment round, or creating a cleaner structure for family ownership. For international founders, a RAK ICC company can sometimes provide a neutral corporate layer above operating subsidiaries in different countries.

The holding plan should be designed before incorporation. Key decisions include the shareholder, the source of funds, the director profile, the expected dividend path, and the future exit route. If the company will hold shares in an operating business, the operating company documents should allow that ownership. If it will hold real estate, the property authority, developer, lender, and project rules must be checked before any sale contract is signed.

A good holding structure is usually boring on paper. It has a clear ownership chain, documented transfers, board resolutions for acquisitions and disposals, and supporting valuations where appropriate. A weak holding structure is the opposite: assets are moved in informally, contracts remain in the individual owner’s name, and the company is added only after a bank, buyer, or tax authority asks questions.

The strongest holding plans also think ahead to liquidity. If the asset is sold, where will the proceeds go? Will dividends be paid to the shareholder? Will another acquisition be made? Are there foreign tax consequences in the shareholder’s home country? A RAK ICC company may simplify some parts of the ownership chain, but it does not erase tax or reporting obligations elsewhere.

Using a RAK ICC company as an SPV

An SPV, or special purpose vehicle, is meant to do one thing. That one thing might be buying a property, entering a joint venture, holding a single investment, issuing shares to co-investors, or isolating a project from other assets.

The discipline of an SPV is what gives it value. If the company is created to hold one asset, it should not also start receiving unrelated consulting income, lending money to family members, or signing contracts outside the project. Mixing purposes weakens the liability ring-fence and creates confusion for banks, courts, tax advisers, and future buyers.

A RAK ICC SPV can be especially useful where investors want limited liability around a defined commitment. For example, a group of investors may prefer to hold a single asset through one company rather than through personal co-ownership. A founder may want a clean acquisition vehicle for a share purchase. A property investor may want to separate one real estate exposure from personal assets and other holdings.

The SPV file should answer four questions clearly: what does the company own, what obligation has it accepted, who funded it, and who has authority to sign? For higher value transactions, the answers should be reflected in shareholder agreements, board minutes, banking records, capital contribution evidence, and contract approvals.

For UAE property investors, the timing is critical. The SPV should usually be considered before signing the acquisition documents, not after personal liability has already been created. This is why many investors review the legal architecture for using an SPV to cap off-plan liability before committing to a purchase.

Using a RAK ICC company in an asset plan

An asset plan is broader than a company setup. It looks at control, benefit, succession, protection, tax, reporting, and liquidity. A RAK ICC company can be one component of that plan, but it is rarely the whole plan by itself.

For private clients, the question is often not only how to own an asset today. It is also who should manage it if the founder is unavailable, how heirs or beneficiaries should benefit, whether assets should be separated by risk type, and how future sales or distributions should be approved.

In some cases, a RAK ICC company may sit below a foundation, trust, family holding company, or other wealth planning structure. For example, the upper vehicle may define governance and succession, while the RAK ICC company holds a portfolio, property interest, or operating company shares. Alldren’s article on RAK ICC Foundations for family office structures explores this approach in more detail for private wealth planning.

Asset protection should be understood carefully. A company can separate ownership and liability, but it is not a magic shield against existing creditors, fraudulent transfers, tax claims, family disputes, or poorly documented funding. The structure is strongest when it is established before problems arise, funded transparently, and operated consistently with its stated purpose.

Choosing the right RAK ICC structure

Not every RAK ICC plan needs a complex vehicle. Many holding or SPV cases can be handled with a standard company limited by shares. More complex cases may justify a restricted purpose company, a segregated portfolio company, or a company owned by a foundation.

| Structure type | Where it may help | Planning note |

|---|---|---|

| Company limited by shares | Straightforward holding or single asset ownership | Often the simplest option when there is a clear shareholder and asset purpose |

| Restricted purpose company | Transactions where counterparties want a tightly defined corporate purpose | The scope should match the transaction documents and financing expectations |

| Segregated portfolio company | Situations where multiple portfolios need separation under one corporate umbrella | Governance must be precise, because records and contracts need to identify each portfolio clearly |

| Foundation plus company | Succession, family governance, and private wealth planning | The foundation governs control and benefit, while the company may hold specific assets |

The more sophisticated the form, the more important the governance becomes. Complexity is not automatically better. A structure that cannot be explained to a bank, buyer, auditor, trustee, or family member may create more risk than it solves.

Banking, tax, and compliance realities in 2026

A RAK ICC company should be planned with banking and tax in mind from the beginning. Banks increasingly focus on substance, source of funds, source of wealth, control, and the commercial rationale for each entity in the chain. A clean incorporation certificate is not enough.

For banking, expect questions such as: why was the company formed in RAK ICC, who ultimately owns and controls it, what assets will it hold, what transactions will pass through the account, and how were the assets funded? If the company will receive dividends, sale proceeds, rental income, investment distributions, or capital contributions, prepare evidence before the bank asks.

For tax, do not assume that offshore means outside the UAE corporate tax system. The UAE corporate tax regime applies based on the law and the entity’s circumstances, and UAE incorporated juridical persons should take registration and filing analysis seriously. The UAE Federal Tax Authority corporate tax portal is the main public source for current rules and guidance, but company-specific advice is essential.

The practical compliance file should include more than registry renewal documents.

| Workstream | What to prepare | Why it matters |

|---|---|---|

| Beneficial ownership | UBO details, ownership chart, identity documents, control explanation | Required for compliance and bank due diligence |

| Accounting records | Bank statements, invoices, contracts, asset records, capital contribution evidence | Supports tax filings, audits, valuations, and future exits |

| Governance | Board resolutions, shareholder approvals, signing authorities, minutes | Shows that the company acts separately from its owners |

| Tax analysis | UAE corporate tax registration review, foreign tax review, transfer pricing where relevant | Prevents surprises when income, exits, or distributions occur |

| Annual maintenance | Registered agent renewal, registry filings, compliance updates | Keeps the company in good standing |

Substance is also a practical issue even where the company is not an operating business. If all decisions, records, directors, bank accounts, and assets point somewhere else, foreign authorities or banks may challenge the company’s role. The answer is not to add artificial substance. The answer is to make the structure truthful, documented, and proportionate to its purpose.

The due diligence file banks and counterparties expect

A well prepared RAK ICC company should be able to explain its story in one clean pack. That pack will differ by transaction, but the core themes are consistent.

Banks and counterparties commonly expect:

- A group chart showing shareholders, directors, subsidiaries, and beneficial owners.

- Passport, address, and background information for controlling persons.

- Evidence of source of wealth and source of funds.

- Contracts, share purchase agreements, property documents, or investment statements linked to the asset.

- Board resolutions approving key transactions and account opening.

- A short business rationale explaining why a RAK ICC company is being used.

This is where many structures succeed or fail. The legal vehicle may be valid, but the file may not be bankable. If a bank cannot understand the source of funds, expected activity, or control structure, the account opening process can stall regardless of the registry.

A practical planning sequence before incorporation

Before forming the company, work through the structure in the order a bank, tax adviser, and future buyer would review it.

- Define the purpose of the RAK ICC company in one sentence.

- Identify the exact assets it will hold and confirm they can legally be held by that type of vehicle.

- Decide who should own the company and whether a foundation, trust, or corporate shareholder is needed.

- Select directors and signing authorities who can support real governance.

- Map the money flows, including capital contributions, dividends, rental income, investment returns, and sale proceeds.

- Prepare the bank story, including source of funds and expected transaction activity.

- Review UAE and foreign tax obligations before the first asset transfer.

- Build a compliance calendar for renewals, records, board approvals, and tax filings.

This sequence is slower than buying a shelf structure without analysis, but it is far safer. A RAK ICC company is most valuable when the setup mirrors the real commercial and family objectives behind it.

Common mistakes to avoid

The first mistake is using a RAK ICC company as a generic offshore box without defining its purpose. If it is a holding company, let it hold. If it is an SPV, keep it single purpose. If it is part of an asset plan, document the succession and control logic.

The second mistake is assuming that privacy means invisibility. Corporate information may not be publicly visible in the same way as some onshore registries, but banks, registered agents, regulators, tax authorities, and courts can require information. Legitimate privacy is about orderly structuring, not concealment.

The third mistake is signing asset contracts personally and trying to insert the company later. This is especially risky for property, financing, and co-investment deals. Counterparty consent, registration rules, taxes, fees, and liability may all change once the wrong party has signed.

The fourth mistake is ignoring the shareholder’s home country. A UAE company may be valid under UAE law while still triggering controlled foreign company rules, reporting duties, inheritance issues, or tax consequences elsewhere.

The fifth mistake is under-documenting family or co-investor arrangements. If multiple people are economically involved, the structure should define contributions, voting, exits, death or incapacity, disputes, and distributions. A company alone does not replace a proper agreement.

When a RAK ICC company is not the right answer

RAK ICC is not ideal for every UAE plan. If you need to trade actively in the UAE, employ staff, obtain UAE residence visas directly through the company, run a regulated financial activity, provide local services, or present a strong operating substance profile, a free zone or mainland company may be more appropriate.

It may also be the wrong answer where the asset authority, lender, developer, or target company does not accept RAK ICC ownership. For example, real estate ownership must be checked against the relevant emirate, project, developer, and registration rules. Do not rely on general statements that companies can own property. Verify the specific asset before signing.

Finally, RAK ICC may not solve banking if the business rationale is weak. A bankable structure is one that can explain why it exists, where the money came from, who controls it, and what activity is expected.

How Alldren helps structure RAK ICC plans

The best time to fix a structure is before incorporation. Alldren helps clients assess whether a RAK ICC company fits the objective, how it should be owned, what compliance file is needed, and whether a wider UAE structure is required for operations, banking, residence, bookkeeping, or tax registration.

That includes practical support around company setup and structuring, ongoing compliance management, corporate governance, bank account opening support, UAE residency planning where an eligible structure is required, bookkeeping, tax registration, and nominee director solutions where appropriate. The aim is not just to register an entity. The aim is to engineer a corporate structure that remains understandable, compliant, and usable.

Frequently Asked Questions

Can a RAK ICC company trade in the UAE? A RAK ICC company is generally not used as a local UAE operating company. If you need to invoice UAE customers, hire staff, lease an office, or obtain visas directly through the business, you should consider an appropriate free zone or mainland structure.

Is a RAK ICC company tax-free? Do not assume that. UAE corporate tax, foreign tax rules, reporting duties, and exemptions depend on the facts. A RAK ICC company should be reviewed for UAE registration, filing, and tax treatment before assets or income are routed through it.

Can a RAK ICC company own property in Dubai or elsewhere in the UAE? It may be possible in specific cases, but it depends on the emirate, project, developer, property authority, lender, and transaction documents. Verification should happen before signing a sale and purchase agreement.

Is a RAK ICC company good for an SPV? It can be, especially where the goal is to isolate one transaction, asset, or investment. The SPV should have a narrow purpose, clean funding evidence, proper resolutions, and contracts signed in the correct company name.

Does a RAK ICC company provide UAE residence visas? Not directly in the way a suitable free zone or mainland operating company may. If residency is part of the objective, the RAK ICC company may need to be combined with another UAE structure.

Can a RAK ICC company be used for succession planning? Yes, it can form part of a succession plan, often alongside a foundation, trust, shareholder agreement, or family governance documents. The company alone should not be treated as a complete estate plan.

Build the structure before you incorporate

A RAK ICC company is most effective when it is designed around a clear purpose: holding, SPV isolation, or asset planning. The legal form, ownership chain, banking file, tax analysis, and governance records should all support that purpose.

If you are considering a RAK ICC structure, speak with Alldren before the company is formed or before the asset is transferred. A short structuring review at the beginning can prevent expensive corrections later.